Eliminating Simulation Bias in Fractional Models for Financial

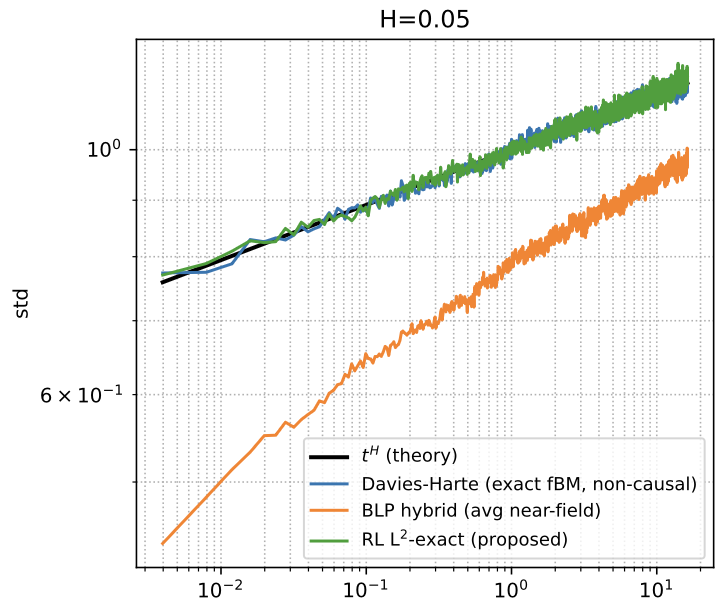

Financial markets are shaped by complex volatility patterns that standard models often fail to reproduce. Rough volatility models capture these fine-scale effects, but their accuracy depends entirely on how the underlying fractional processes are simulated. Our new L2-Exact Riemann–Liouville (RL)…